Why Ignoring Asia's Payment Challenge is a Big Mistake ?

ASIA BUSINESS FACTSBUSINESS TIPS

Alan Wong

3/5/20246 min read

In Asia, the evolution of payment systems is facing crucial challenges, reshaping how consumers and businesses transact.

From the surge in digital payments to the complexities of cross-border payments.

As Asia moves towards a more integrated financial landscape, understanding these challenges is key to navigating the future of payments in this dynamic region.

What is Cross-border Payment in Asia?

Cross-border payments in Asia refer to financial transactions where the payer and

recipients are based in different countries within the region.

This process is facilitated through various digital platforms, allowing for seamless transactions across national borders.

Recent initiatives aim to integrate payment systems across ASEAN countries, enhancing efficiency and

reducing reliance on traditional banking methods and foreign currencies.

This integration supports economic growth and simplifies payments for businesses and

consumers alike, marking a significant step towards financial inclusivity and connectivity in Asia.

Payment Methods in South Korea

South Korea's payment landscape is highly advanced, with a strong inclination towards cashless transactions.

Among the popular methods, credit and debit cards dominate, while mobile payments have seen a rapid surge with apps like KakaoPay and Naver Pay leading the market.

Additionally, South Korea's unique T-money and Cashbee cards cater to public transport and retail needs, further embedding cashless habits into daily life.

These diverse options reflect South Korea's tech-forward approach, offering convenience and efficiency in financial transactions.

What are the Payment Methods in Asia?

Asia's payment landscape is a tapestry of traditional and modern methods.

Cash transactions remain prevalent, but there's a significant shift towards digitalization.

Traditional bank transfers, credit and debit card usage vary by country but are universally recognized.

Mobile payments are on the rise.

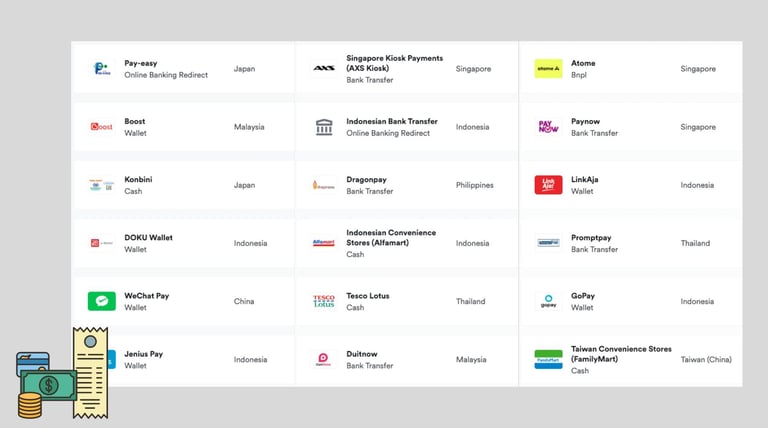

Payment Methods in Southeast Asia

In Southeast Asia, cash is still king, but mobile and digital payments are rapidly gaining ground.

The adoption of QR code payment systems like QRIS in Indonesia, DuitNow in Malaysia, and PromptPay in Thailand illustrates this shift towards tech-savvy transaction methods.

Other than that GoPay in Indonesia, GCash in the Philippines are two notable examples of mobile wallets.

These platforms cater to a digitally connected population, offering convenience and security.

Payment Methods in China

China is a global leader in digital payments, with mobile wallets like Alipay and WeChat Pay dominating the market.

These platforms offer an array of services from online purchases to bill payments, with QR codes facilitating most transactions.

Payment Methods in Japan

In Japan, some popular cashless payment options include credit and debit cards, mobile payment apps like PayPay, Line Pay, and Rakuten Pay, as well as e-money cards such as Suica and Pasmo which are widely used for transportation and retail purchases.

These methods cater to a tech-savvy population and are designed to offer convenience and efficiency in various transactions, making them integral to daily life in Japan.

For a business consultant who understands the depth of Asia's business environment, reach out to us, ToAsia.biz, and take the first step towards your success in the Asian market.

Payment Methods in India

India's payment landscape is diverse, catering to its vast and varied market.

Digital transactions have become increasingly popular, with UPI (Unified Payments Interface) leading the charge, allowing instant bank-to-bank transfers via mobile apps.

Other prevalent methods include traditional credit and debit cards, mobile wallets like Paytm, Google Pay, and PhonePe, which offer a range of services beyond simple transactions.

This blend of traditional and modern payment options reflects India's unique position at the intersection of technology and tradition in the financial sector.

The future of payments in Asia is poised for continued growth and innovation, driven by consumer demand and technological advancements.

What are the Payment Challenges in Asia? Security

Security remains a paramount concern in Asia's payment landscape, with fraud and cyber-attacks posing significant risks.

The diverse regulatory environments and varying levels of digital infrastructure across countries complicate the implementation of standardized security measures.

How to Solve Security Challenges in Payment?

To combat security challenges, robust authentication measures, encryption protocols, and fraud detection systems are essential.

Implementing advanced technologies such as biometric authentication and tokenization can enhance security while ensuring a seamless user experience.

Additionally, continuous monitoring and analysis of transaction data can help identify and mitigate potential security threats in real time.

Foreign Currency Transfer Rate in Cross-border Payment

Foreign currency transfer issues are one of the payment challenges in Asia.

With diverse economies at different stages of development, fluctuations in currency values and transaction costs can affect cross-border payments and trade.

The dependence on major currencies like the U.S. dollar for transactions adds complexity, as does ensuring favorable exchange rates in a region seeking more financial autonomy through systems like QR code payments.

These challenges emphasize the need for regional financial integration to mitigate reliance on external currencies.

How to Solve FX Challenges in Cross-border Payment?

Cross-border payments often encounter foreign currency transfer challenges, including fluctuating exchange rates and high transaction fees.

Solutions like Airwallex offer integrated FX capabilities that provide competitive transfer rates and lower fees compared to traditional banks.

By leveraging technology and automation, platforms like Airwallex streamline the FX process, enabling businesses to conduct cross-border transactions more efficiently and cost-effectively.

Real-Time Payment Challenges

Millions in rural areas remain unbanked, lacking access to formal financial services.

This poses a significant hurdle to economic development and participation in the digital economy.

In countries like India, the uptake of real-time payments is soaring, signaling a shift towards immediate digital transactions.

This move is facilitated by widespread internet usage and a preference for online banking.

How to Solve Real-Time Payment Challenges?

Real-time payments present challenges related to infrastructure, interoperability, and security.

Addressing these challenges requires the development of robust real-time payment systems that are scalable, secure, and interoperable across different networks and jurisdictions.

Solutions like Airwallex offer super-fast payment capabilities that facilitate instant fund transfers, providing businesses with greater flexibility and liquidity management options.

The Final Word: Embracing the Future

Asia's payment landscape is undergoing a radical transformation, driven by a confluence of technological advancements, changing demographics, and evolving consumer preferences.

Understanding these challenges and opportunities is crucial for businesses looking to tap into this dynamic market.

By staying informed and adapting to the evolving landscape, businesses can unlock the immense potential of Asia's growing digital economy.

Sign up Airwallex for your first $100,000 of foreign exchange free!

Alan Wong is founder of ToAsia.biz and a startup mentor with over 20 years of professional experience managing software, Saas and consulting services MNCs.

About Author

Copyright © 2026 ToAsia.biz

We lead your business to Asia

Our Business Growth Experts help SaaS businesses achieve growth in Asia and become profitable FAST.

Send us a message via WhatsApp